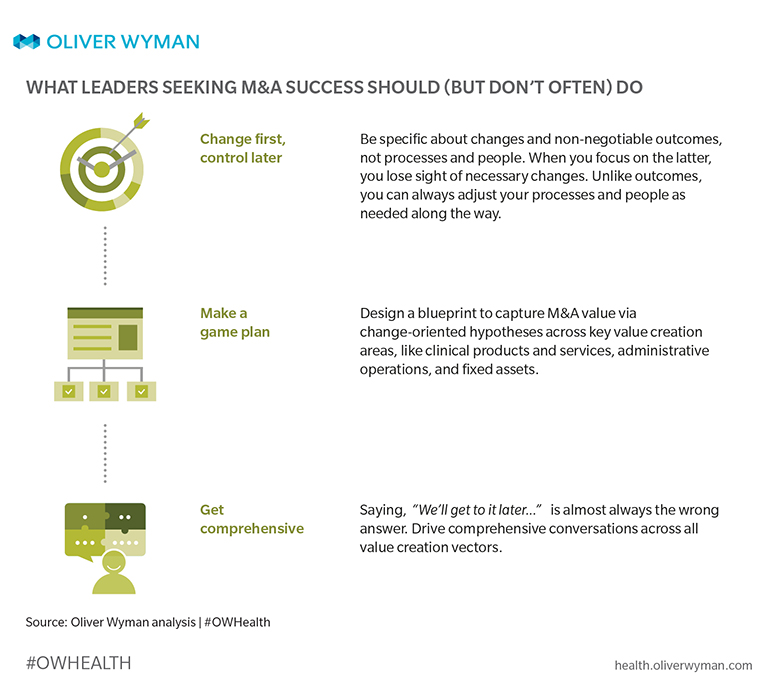

Now You See Us, Now You Don't

Healthcare organizations and industry players alike turn to mergers and acquisitions (M&A) as a fast track to innovate, scale, and maintain market relevance. Press releases promise golden possibilities – lower costs, enhanced experiences, better clinical outcomes, and healthier populations. In short, M&A promises a new world. So why does M&A regularly disappoint on delivering on those promises – with some transactions actually destroying value? Change is hard. In many cases, change goes against current incentives or business models. Execution fails due to a lack of planning and an overemphasis on control (such as deciding who will take which leadership role) rather than what modifications can command success. “When the partners depend on each other and also have bargaining power over each other, they often end up haggling over the surplus after the fact,” said Benjamin Gomes-Casseres in Harvard Business Review. “It’s kind of like sumo wrestlers trying to dance. For bystanders, it’s often not pretty.”

Analyzing a Smoke and Mirrors Market

Two big flavors of M&A are present today: traditional transactions emphasizing advantages through size and scale-based efficiencies (such as negotiating power and sharing common resources and investments). And, nontraditional combinations, bringing novel organizations together to disrupt how and what services are delivered. Sometimes, the latter ends up changing how the whole market functions.

Despite market excitement over each transaction’s future impact, healthcare M&A transaction results often fall short compared to non-healthcare transactions. “Very few people have actually gotten any value out of [M&A deals],” said A. Marc Harrison, Intermountain Healthcare Chief Executive Officer. In comparison, non-healthcare industries have very different outcomes when similar organizations come together.

One such example is Proctor & Gamble’s (P&G’s) purchase of Gillette. Although both companies operated successfully in their respective consumer product spaces, by extending Gillette’s shaving technology across P&G-owned women’s brands and integrating their lotions and deodorants into P&G’s product line, the two brands collectively created an innovative experience and product suite. Are we seeing this type of value creation in healthcare? The answer is an emphatic no.

Today’s M&A value creation tends to come from “fall out of bed” impact that stems from size and the negotiating clout that accompanies magnitude. That, however, is short-lived, just the tip of the iceberg. Full value extraction means making bold choices to optimize and introduce a new service and product mix. Shared services bring valuable scale across all facets of the operation, from supply chain to finance to information technology. New technical capabilities link operations.

A critical question for leaders: What can we learn from industries beyond healthcare where M&A activities have generated greater returns for shareholders, customers, and broader communities?

Purposeful A to Z Integration Means No Stone's Left Unturned

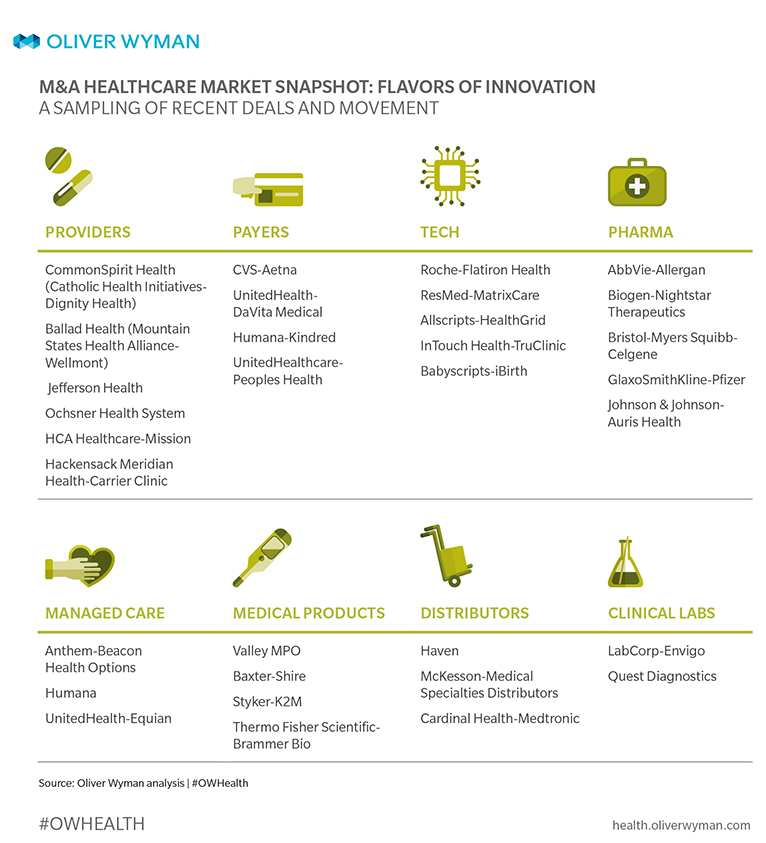

Traditional, scale-oriented mergers succeed by bringing a laser focus to operations and serving consumers. This means critically evaluating a mix of services and products and, where offerings are provided, optimizing newly formed options into innovative consumer-facing offerings. Payers have been on a consolidation track for a while now and have had success in using acquisitions of health plans and competitors to gain access to new markets. Payers’ M&A playbooks emphasize rationalizing products and services, streamlining of operations for end- consumers, and designing for aggregated market demand.

Consolidation among providers has been the subject of many a headline in recent years. While many still struggle to integrate, there are some bright spots among those organizations prepared to make use of their newly acquired assets and capabilities in braving a new future. Some examples include:

- A group of rural, community hospitals acquired by an academic medical center that brought underserved communities enhanced access to critically needed cardiovascular services. Despite market pushback, leadership kept its focus, engaging its team and community; the result was lower cost, better care, and improved community relationships.

- After many years of functional integration (such as back office and common staffing roles), a large Midwest health system changed its service mix and care delivery infrastructure. This meant transforming current care sites into purpose-built care facilities (such as getting an orthopedic hospital, a geriatric outpatient hospital, and main tertiary high-end facility to work together in offering the lowest cost/greatest value experience) to meet today’s clinical and consumer needs in a specialized manner; the result was optimized cost structure via specialization and improved quality through concentration of clinical capabilities and volume.

These examples are perhaps still too nascent and isolated in comparison to bolder possibilities. Having worked intimately with these organizations, change requires strong commitment to future visions and a willingness to stay the course. Not to mention – managing diverse stakeholders through the journey, including clinician partners.

Tomorrow's Non-Traditional M&A's Focus? Create New Configurations (While Chaos Surrounds You)

Unlike M&A between similar organizations, non-traditional M&A requires a nuanced approach to design and integration. Otherwise, healthcare leaders face risk of “organ rejection.” The reason is non-traditional M&A involves heterogeneous combinations of different business models and market perspectives. Despite the challenge, the desire for disruption has fueled non-traditional market tie-ups. That said, there are examples of unique value-creation formulas:

- Amazon and PillPack – New Market Entry and Exploration. This collaboration promised the opportunity for Amazon to venture into a new pharmacy-distribution market. However, Amazon did not completely subsume PillPack’s virtual pharmacy operation and identity, recognizing the importance of independence during the experimentation period.

- Unitedhealthcare and Optum – Vertical integration. UnitedHealthcare, directly and through its subsidiary, Optum, had a similar approach when acquiring care delivery capabilities across select markets (like DaVita).

- Advisory board Company and Optum – Force Multiplier. At first glance, Advisory Board Company’s sale to Optum may perhaps be a head-scratcher, given Advisory Board’s core identity as a research, consulting, and technology firm. But through Advisory Board’s acquisition, Optum may gain new channels to engage the market and fuel growth. Alternatively, Optum could integrate Advisory Board’s broad provider understanding and accelerate OptumCare’s market role in serving more patients with Medicare Advantage plans, as well as other elderly patients. There are likely many layers of additional value creation being addressed.

- Iora health and Flatiron health – Strategic investments. Consider how some organizations, like Iora Health, which runs a network of primary care clinics around the US, are investing early for a seat at the table. Iora, which raised $100 million Series E financing in 2018, aims to become one of the biggest players in digital healthcare and non-traditional health systems by advancing its collaborative care model, which involves a team of doctors, nurses, and health coaches tracking each patient’s health with the aid of Iora’s software platform. Or take Flatiron Health, a venture acquired by Roche in 2018. Flatiron Health has become a key driver in health technology. In addition to its OncologyCloud platform which includes electronic medical record for oncology, advanced analytics, a patient portal, and integrated billing management, Flatiron’s platform serves as an aggregating data resource that enables oncology researchers to develop real-world insights. Iora and Flatiron made key strategic “bets” and provided an environment to fully test and validate their market hypotheses. How it integrates into the overall business is to be determined.

These examples cut across the industry but share commonalities. Rather than consuming the whole, as is common in purely built-for-scale deals, all involve nuanced approaches. Here, integration makes room for cohesion and independence instead of situations where teams suddenly working with larger behemoths find themselves become more stifled with each passing day. As organizations consider these transformative deals, there are several “baseline” considerations:

- Assess disruption readiness internally. Understand your cultural readiness to tackle top challenges hindering progress. When working in healthcare, an industry where disruptive value comes from people, intellectual capital, and resulting innovations, the last thing you want to do is squander your source of competitive advantage. Align your teams towards change or else you will find yourself rowing in circles as others pass you by.

- Beef up scenario planning and integrate it into the transaction thesis. Unlike traditional plays, be nimble and prepared for external market shifts and the competitive landscape. Scenario plan rigorously to validate key assumptions (such as valuation shifts, market reaction, and impact on uptake of new concepts, unanticipated consumer response, scalability challenges, and more).

- Be relentlessly intentional and focused. M&A is, in short, a major time investment, demanding your full attention, not partial interest. Developing an M&A strategy – while trying to disrupt your business at the same time – is about prioritizing. Don’t venture along an M&A voyage half-halfheartedly. Doing so will mean M&A will only serve as a distraction that puts you on the fast-track to value annihilation.

- Recognize structure is merely a shell. Joint ventures don’t equal de-risking. Non-traditional tie-ups without balance sheet implications may initially seem low-risk, but that’s purely from a capital commitment perspective. The truth is, the amount of time, resources, and organizational attention spent on poorly constructed joint ventures causes severe value decline. The stakes are the same regarding how many people and how much time is needed to make a non-asset M&A (like joint ventures or affiliation) successful.