Projected Medical Trends and Value-Based Opportunities Amidst ACA Uncertainty

Medical trends are not the prime cause of rising premiums in the Affordable Care Act market. That is one of the key takeaways from the latest Oliver Wyman Carrier Trend Survey, a semi-annual survey with over 75 insurance company participants, which found medical trends in the Individual health insurance market remained relatively steady in January 2018. This survey collected medical pricing trends that carriers include in their rate development when estimating their health insurance premium rates. (All participants in the survey receive a copy of the report prior to its posting.) The carriers responding to the group and individual markets represent over 109 million members in their blocks of business.

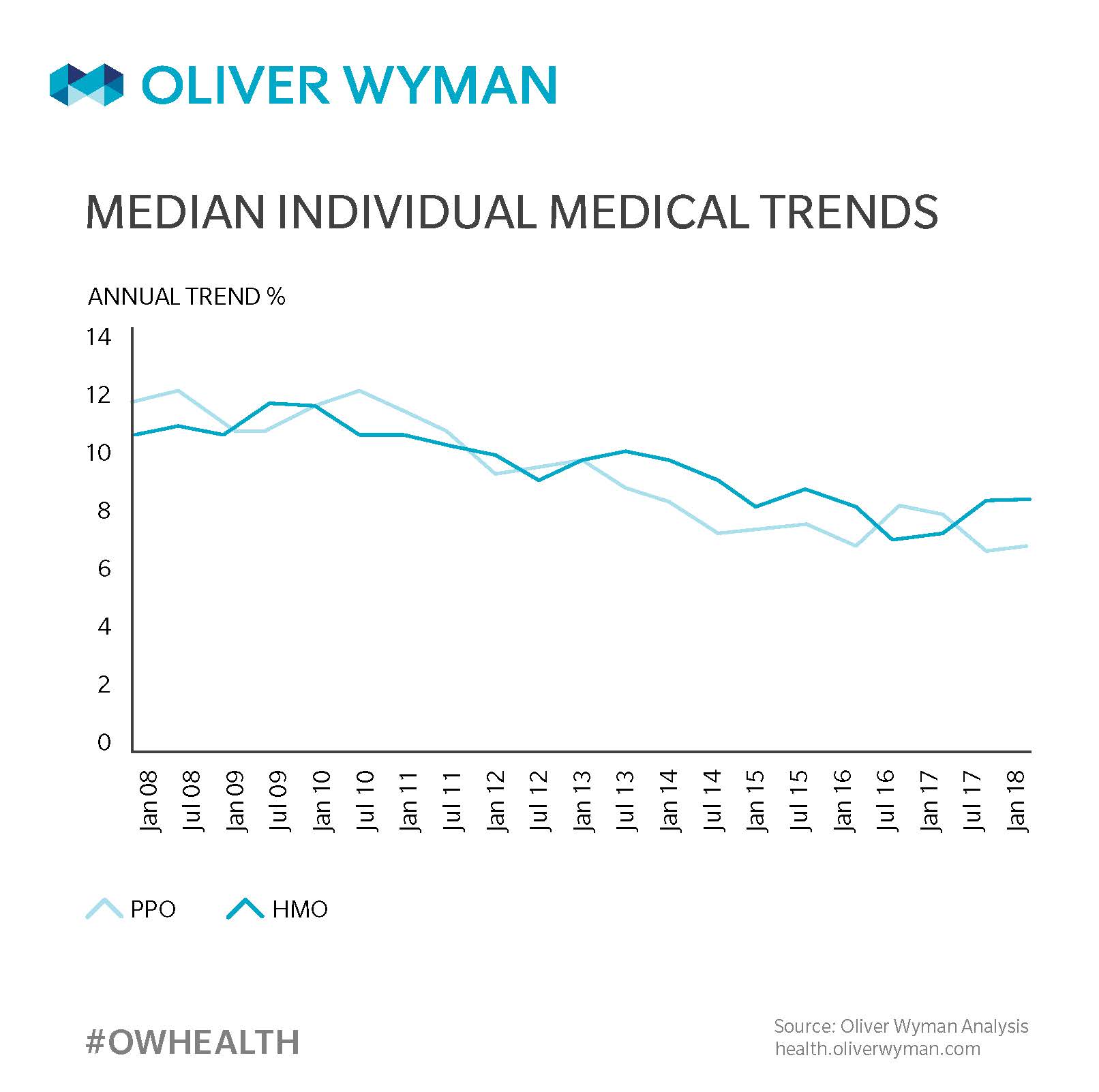

Even with notable uncertainty surrounding the fate of the Affordable Care Act at the time of the survey, carriers’ perspectives on medical trends were clear. Individual medical trends remained stable going into 2018 for the most popular types of plans – preferred provider organizations (PPO) and health maintenance organizations (HMO) – with trends converging between 6 percent to 8 percent in this market.

Interestingly, our historical survey shows carriers have been using pricing trends in this range since July 2014 to develop rates, further demonstrating items other than trend are contributing to the increase in premium rates for this market, such as population changes, guaranteed issue requirements, the lack of cost sharing reduction funding, and the elimination of the individual mandate. Given that rates in 2018 increased on average between 26 and 28 percent, that leaves approximately 20 percent of premium increases to non-trend factors.

The graph below shows the historical changes in this market over the past decade:

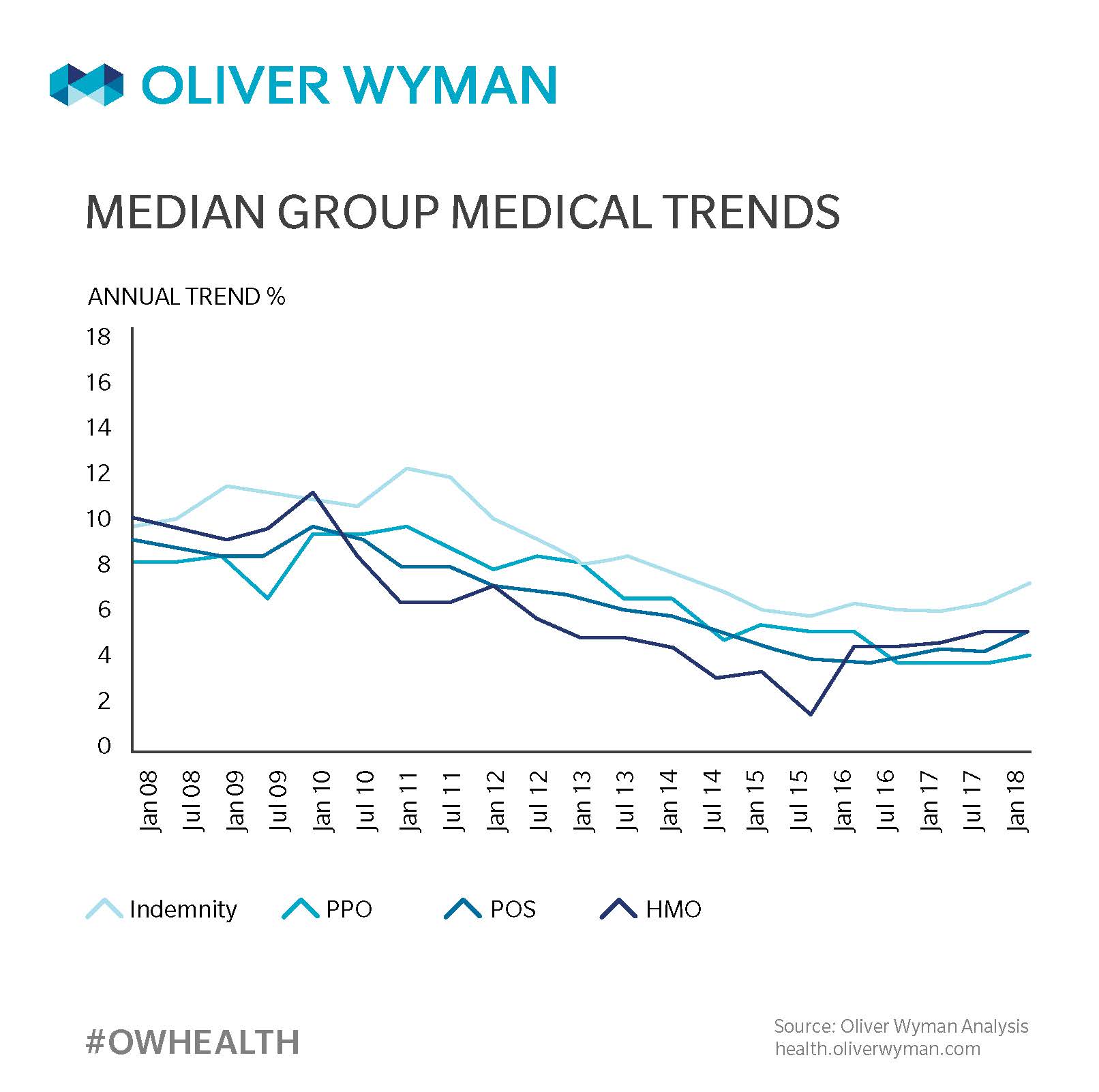

Medical trends in the group health insurance market (shown in the following chart) increased slightly in 2018 for those products that typically employ less managed care controls, such as Indemnity, PPO, and point-of-service plans. Alternatively, the median trend for Health Maintenance Organization products was essentially unchanged, which potentially reflects the utilization and provider contracting controls they have in place.

Similar to the individual market, the median trends in the group market have converged around January 2016 and have remained between 7 and 9.5 percent. The graph below shows the historical changes in medical pricing trends in the group health insurance market over the last decade:

In both cases, trends have declined over the 10-year period into single digits. However, it appears trends have been more recently flattening rather than continuing to decline. Even with these trends remaining constant, they continue to be significantly higher than Consumer Price Index, driving the need for alternative approaches to make healthcare more affordable.

There is currently a relatively small number of value-based efforts in place. As other market forces increase, such as the move to value-based reimbursement for providers, narrower provider networks, and more effective care management techniques, it will be interesting to see the impact these initiatives have on medical trend, and if they can bend the trend.